Research project: Conceptualizing Popular Financial Annual Statements (PFiAS)

“The primary function of governments and other public sector entities is to provide services that enhance

or maintain the well-being of citizens and other eligible residents”

(International Public Sector Accounting Standards Board (IPSASB) Conceptual Framework (CF) 2.7).

Background

General Purpose Financial Statements (GPFS) are an important means of governments to discharge accountability towards citizens for their actions or decisions in terms of raising or using resources entrusted to them (e.g. by collecting taxes) for the provision of services. But, academics argue that citizens are not interested in GPFS information and do not use it.

To this background, means and actions are discussed for raising interest of citizens in politics and for facilitating and encouraging a political dialogue. In particular, the idea of a popular report stands out. The idea is not new but has a long tradition in North America since the 1990s. Traditionally, “popular … reporting is a means … to provide – mainly – … information to citizens in a concise and easily understood manner aiming at enhancing citizens’ understanding of public … matters” (Cohen & Karatzimas, 2023 with reference to Stanley et al., 2008) to the end of enabling political engagement, deliberation and interest of citizens.

From another perspective, Popular Reports have two functions. They offer a means for informing citizens on (selected) GPFS content and are a means for public relations aiming at image improvements, also with respect to the attractiveness of (future) residents and businesses (e.g. companies) and to the commitment or sense of belonging of residents and businesses (implicitly Küting & Hütten, 1996; Cohen & Karatzimas, 2023).

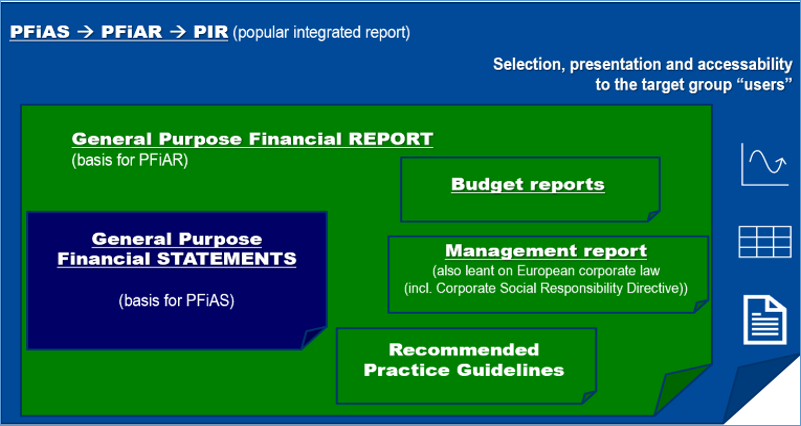

Lately, popular reports are also discussed in European countries (e.g., Greece and Italy). On the one hand, recent research extends the scope of Popular Reports from Popular Financial Annual Reports (PFiAR; covering financial budget and/or FS information) to Popular Integrated Reports (PIR; also including non-financial (i.e. sustainability) information) (see also Figure 1). On the other hand, presentation (e.g., the use of infographics) and accessibility issues (inter alia in the light of digitalization: e.g. push options like e-mail or pull-options like webpages) are discussed. Nevertheless, to the best of our knowledge, no attempt has been made to conceptualize citizen-centred Popular Financial Annual Statements (PFiAS) derived from IPSAS GPFS at the state Level. This is the application-oriented research gap, we address in our project, with respect to the German state (Bundesland) Hesse.

Figure 1: Scope of PFiAS

Notabene: PFiAS is part of a broader research agenda towards PFiAR or PIR.

Selected research steps – so far (June 2024)

Literature reviews

- Users, information needs and use of general purpose financial statements (GPFS) in the public sector: Overview of international research

- Citizen-oriented alternative financial reporting in the public sector: Overview of international research

- Use of visual aids in financial reporting: Special features for citizen-oriented government accounting

Empirical research

- Citizen-oriented financial reporting in the German federal states: Implications for reporting to selected target groups using the example of the IPSAS financial statements of Hesse (e.g. Students, Senior citizens; parents; persons without children in the household)

- Citizen-oriented financial accounting of federal states - Derivation of citizens' interests on the basis of interviews

- Citizen-oriented financial accounting of federal states - Derivation of citizens' interests on the basis of a survey

Conceptual research

- Citizen-oriented accrual-based financial reporting by German federal states: Relevant information and indicators of the statements of financial position, financial performance, cash flow by the example of the IPSAS financial statements of Hesse

- Citizen-oriented accrual financial reporting in the public sector: Status quo and implications of research on selected theories (e.g. cognitive load, reader-response theory)

References:

Cohen, S. & Karatzimas, S. (2023). Users in preparers' shoes: mobilizing the sense of belonging in popular report development in local governments. Journal of Public Budgeting, Accounting & Financial Management. 35. 199-218. 10.1108/JPBAFM-03-2023-0038.

Küting, K. & Hütten, C. (1996). Der Geschäftsbericht als Publizitätsinstrument, BB 1996, S. 2671

Stanley, T., Jennings, N. & Mack, J. (2008). An examination of the content of community financial reports in Queensland local government authorities, Financial Accountability & Management, Vol. 24 No. 4, pp. 411-438.

Yusuf, J.-E., & Jordan, M. M. (2012). Effective popular financial reports: The citizen perspective. Journal of Government Financial Management, 61(4). 44.